Financial-literacy advocates in New Mexico are upping the ante in anticipation of the 2021 state legislative session. They claim the last state legislation didn’t go far enough to protect consumers and they collectively aim to continue tackling predatory lending issues.

Legislative Action from 2017

Congress passed several house bills to address short-term loan practices in 2017. The legislation outlawed payday loans. The new bill also:

- Mandated that lenders assess each consumer’s ability to pay back loans,

- Update each loan with new required underwriting, and

- Adhere to new reporting standards and cap interest rates at 175% APR.

Before this legislation, lenders were largely unregulated. Underwriting was frequently unclear and inconsistent, and interest rates were known to be as high as 1,500% APR.

Not Far Enough

Small-loan companies lobbied against the 2017 regulation effort tooth and nail—working to whittle down the final legislation significantly. As a result, many consumer advocates view the resulting house bills as appeasing and unsatisfactory. They argue that it has taken too long to enact and that more meaningful regulation is needed to make an impact.

One of those organizations is the political-advocacy think tank, Think New Mexico. Their goal is to further reduce interest rates to 36% and to make financial literacy classes a graduation requirement for high-school students.

Financial Literacy in New Mexico

High schools in New Mexico are required to offer financial literacy classes. These programs are funded by a required annual fee that loan companies pay.

However, students aren’t yet required to take those courses to graduate. Only 11% of students took a financial-literacy class during the 2019-2020 academic year. There is a good reason for these classes. New Mexico is currently ranked 47 out of 51 as one of the least financially literate states in the U.S., according to Wallethub.

Federal Bureau Overrides State Law

The Consumer Financial Protection Bureau (CFPB) recently revoked provisions of New Mexico’s 2017 regulations, gutting them of most of the punch they packed.

The CFPB rescinds the requirement for lenders to ensure consumers are fit to borrow. It also removed new underwriting and reporting mandates. In its final ruling, the Bureau states that it “is making these amendments to the regulations based on its re-evaluation of the legal and evidentiary bases for these provisions.”

This ruling has rekindled the fire in the fight for many financial-advocacy groups. The New Mexico Center on Law and Poverty issued a scathing response in which it accuses the CFPB of “ignor[ing] extensive public comment” and of conducting unregulated loan-borrowing itself.

Arguments For and Against More Small-Loan Regulations

Opinions vary on how further legislation might affect New Mexico’s lending industry.

Interest-Rate Reductions and Revenue

State representatives like Rep. Patricia Lundstrom have concerns about further regulating short-term lending for options like title loans. She worries that such an aggressive interest-rate reduction could lead New Mexicans to borrow from online lenders, which aren’t regulated like brick and mortar storefronts. Additionally, there are concerns over possibly bankrupting companies and reducing state-licensing revenue.

Considering that the APR used to be 36% before the 1980s’ inflation scare, this argument irks advocates for additional reforms. They claim that returning interest rates to previous numbers will not endanger lenders. Other states have imposed strong regulations without suffering any major losses.

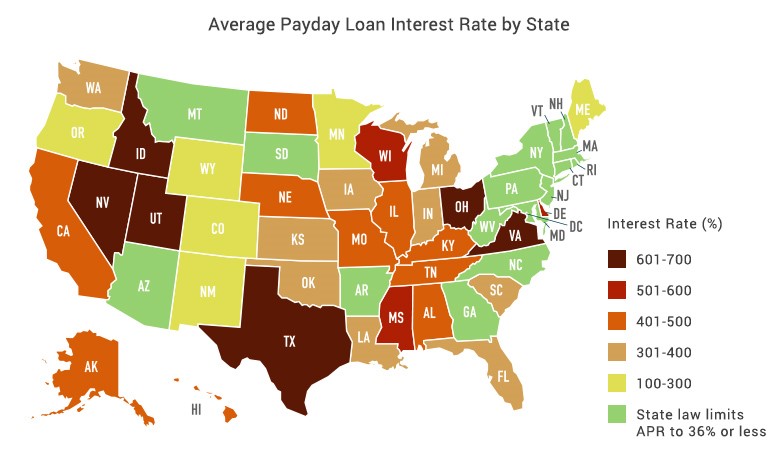

Despite the 2017 legislation, New Mexico is still home to the 3rd-highest interest rate in the country—its 175% APR is five times the national average.

Predatory Lending and Unfair Practices

The “buyer beware” argument outlined by the CFPB says that consumers are responsible for understanding the conditions of their loan before they agree to it.

Ironically, Titlelo.com (a lender that offers title loans in New Mexico) is one of many advocates that are calling for more aggressive legislation. Their argument is that predatory lenders are attracted to states without strict regulations, like New Mexico. Only 15% of short-term lending companies in the state are owned by corporations based in New Mexico. There are 595 small-loan licenses currently distributed throughout the state (as of April 27, 2020), which means there is a store for approximately every 3,800 residents (as a comparison, McDonald’s only has one location per 23,300 residents).

To compound that concern, consumers are especially susceptible to predatory loans during times of economic distress, as we’re currently experiencing due to COVID-19.

A spokesperson for Prosperity Works believes that the 2017 regulations “do very little to address … concerns” over unclear loan terms and lofty fees that can easily trap consumers in a cycle of debt. Currently, 80% of short-term loans in New Mexico are never paid off, but instead refinanced or rolled over.

Awaiting 2021

Congress is reconvening on January 4, 2021, and is expected to continue discussing lending practices next year. So far, there doesn’t seem to be much congressional support for lowering short-term interest rates, but advocates plan to continue their work to protect and educate borrowers of title loans.